ONE goes for US market share ‘Land Grab’ with $20M Capital Raise

We invested in growth stage health tech provider Oneview Healthcare (ASX:ONE) because we saw its potential to modernise and transform healthcare service delivery.

ONE uses cloud technology to provide hospital patients a “virtual care and digital control centre” at their bedside that delivers the best possible patient experience during their stay.

ONE has achieved the early proof points we wanted to see with its newly launched cloud version of its tech and is now seeking market penetration in the US - the most lucrative healthcare market in the world.

ONE has already signed multiple USA based hospitals, including Kingman in Arizona, part of the prestigious Mayo Clinic Care Network, and NYU Langone, one of the top 10 hospitals in the US (who recently publicly endorsed ONE’s technology).

Today ONE announced they have raised $23M in cash that will be used to accelerate sales and adoption, specifically in the US healthcare market (raising announced via two tranches and a share purchase plan)

Our original investment thesis for investing in ONE back in March this year was to:

- See them launch their cloud based version (✅ DONE),

- Prove they can sell the cloud version to new and existing client hospitals (✅ DONE x 3)

- Gain more traction in the USA (✅ DONE), and

- Sell more through partner channels Microsoft and Samsung (🔄 in progress).

Now that ONE has delivered these key proof points on their new cloud tech AND has an early mover advantage, we want to see them acquire more market share, particularly in the large US market.

There are two ways ONE can do this:

- Steady state: At their current pace, with their current modest sales team and marketing budget, self funding through their current revenue and trying to get to an early break even cash flow positive state;

- Fast: Raise capital for an aggressive market share “land grab” by hiring more salespeople and investing more in marketing - the typical model for high growth SaaS companies in the venture capital space.

“Fast” is the strategy ONE has adopted.

We invest in early stage and growth companies seeking 1,000% gains over the long term.

Now that ONE’s product is proven to be successful among customers, raising capital to go for accelerated growth is a strategy we like.

We want to see ONE move fast to secure its early mover advantage, which if they can execute on should see them trading on a higher future revenue multiple.

ONE raised $20M at 27 cents per share (with $3M possible through a share purchase plan to existing holders) that they say will be used for "expansion of sales and marketing capabilities and delivery of new product enhancements".

We read that as get as many users (contracted hospital beds) live, as quickly as possible, and some development resources to ensure their cloud platform can handle the increased uptake that comes with increased sales.

We have seen some tech companies in the past try to raise “land grab” capital too early, BEFORE they have achieved key proof points around sales, adoption and retention. However there is no point ramping up sales and marketing unless you are sure your product is sellable, sticky and the clients adopt it and extend usage.

In our opinion ONE is in the sweet spot to put the foot on the gas in sales and marketing.

We think the amount raised versus the dilution to existing holders is a very good trade off as it will allow ONE to deliver the remaining points (shown in yellow) in our original investment thesis much faster, and we expect the speed of new customer acquisition to be a driver for a share price re-rate (if ONE can execute of course):

We participated in the capital raise and as existing holders will also be applying for shares in the SPP.

With the new funds raised, we have now added the following milestones that we want to see ONE achieve over the next 12 months with the new cash (and will be providing regular updates on how they are progressing against each):

🔲 Double marketing spend (check in next quarterly)

🔲 New USA deal #1 by Feb 2022

🔲 New USA deal #2 by April 2022

🔲 New USA deal #3 by June 2022

🔲 Reach 15,000 contracted beds within 9 months

🔲 Reach 20,000 contracted beds within 18 months

🔲 Cross selling and upselling - new products/integrations sold

(note: these are our personal opinion on what we would like to see as investors in ONE, they have now been added to our revised investment thesis on the ONE company page)

We believe ONE has timed this capital raise well, as it strengthens its balance sheet and solidifies its Enterprise Value with a complementary cash balance. In less complex language, the prospect of future growth in revenue is great - but it needs to be backed by an ability to invest in that growth.

In our view, after this capital raise ONE will be well placed to grow, maintain and enhance its product offering and scale quickly - even if the market enters a rough patch.

Here’s how we see ONE knocking down these new milestones via a new strategy...

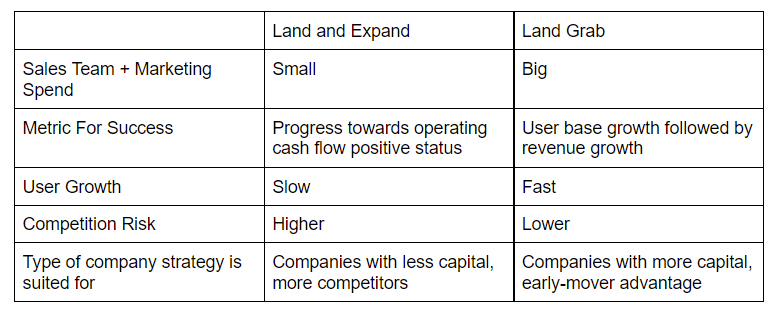

What's a “land grab” in growth stage tech anyway?

In technology (specifically SaaS), a “land grab’ strategy is where a tech company targets rapid user base growth rather than short term profitability.

In our opinion, this works best when the company has proven that it has a product that can be sold AND is retained over time by its early customers.

ONE's increase in capital comes with a change in expectations from investors.

Instead of hitting operating cash flow positive status, investors want to see them grab as much market share as fast as possible, and aggressively ramp up sales and marketing, so they can secure an early mover advantage and become the dominant player in the space.

This is particularly relevant in ONE’s case, as they generally sign large, long term deals and hospitals are sticky customers over the long term - so an investment in a “land grab” now will provide ongoing revenue for ONE for many years to come.

It will also cement ONE’s early mover advantage with the cloud version of its solution.

This is the classic venture capital tech model - where in the early growth stages, the increasing user base is more relevant to investors than short term profitability.

How ONE has been going

Late last week ONE announced a new revenue guidance for FY21 with revenue expected to be between €9.5 ($14.9M) and €10.0m ($15.7M) with H2 revenue ~90% greater than vs H1.

This is a slightly more modest figure than the ~100% revenue growth and $10.4M in H2 that it projected.

ONE also came out with FY22 revenue guidance of between €12.5 ($19.6M) and €14m ($22M).

Based on what we have seen so far, we think this is certainly achievable - we say this given our long-term confidence in management and the product that ONE sells. This will be easier now with a strong cash balance to support the growth.

Before we invested in ONE, we liked that ONE had already delivered $7.8M of Annual Recurring Revenue from 9,259 hospital beds.

They have already proven they can execute complex enterprise sales to large hospitals. The next step is to scale that up.

As of today’s capital raise they have 11,615 beds contracted globally - we want to see them get to 15,000 beds in the next ~9 months.

As we highlighted above, ONE has just raised $20M from institutional investors and there is a further $3M to be raised from a Share Purchase Plan (SPP).

We look forward to seeing ONE ramp sales and marketing with these funds, because at a core level, hospitals and healthcare need to improve service delivery for patients while also reducing the burden on practitioners - particularly in light of the pressures brought on by the pandemic.

As a result, some types of nursing work have attracted nearly 3-5 times more pay. Which highlights how hospitals need to modernise care delivery in order to protect the economics of their system.

ONE has an early-mover advantage and once they convince a hospital to go-live with them the deals are sticky and long-term (typically 3-5 years just for the initial contract). Their customer retention rate is 98%.

But changing the way healthcare is done isn’t easy. Many hospitals move slow and are resistant to change due to tight budgets.

However, once a deal is placed we think both hospitals and patients will find it is the right solution for them. Better, quicker care in a digital medium for the modern hospital.

We’re looking for ONE to make the breakthrough in the US and quickly achieve market penetration with this capital raise in hand.

Marketing spend and the prize on offer

ONE has already shown it can ink major deals. The Kingman deal for instance was worth USD$2.4 million - that’s a decent chunk.

Big deals, small deals, ONE has shown that it is capable of both.

Before today’s capital raise, ONE selling its new cloud product largely on a ‘Land and Expand’ sales model, for which it delivered some early proof points.

But post-capital raise we believe it will transition to a ‘Land Grab’ model, spending on marketing, brand awareness and customer experience to drive more deals, faster.

Here’s how the capital raise can impact their growth though - a big tangible increase in the sales team and marketing.

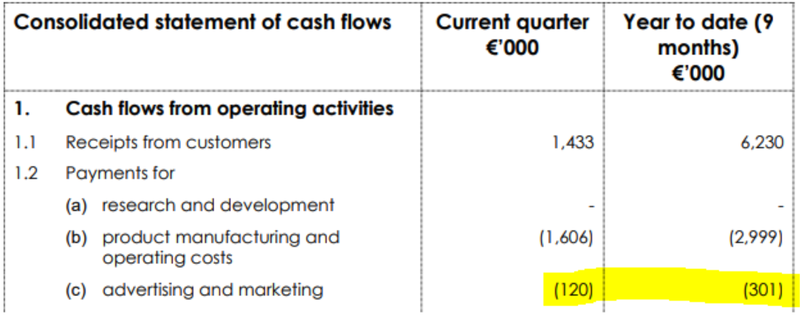

Here is how much ONE spent on advertising and marketing in its latest quarterly:

That’s modest in our eyes compared to other growth stage enterprise SaaS companies YET they still managed to bring in multi million dollar deals.

The $23M from this cap raise should go a long way to getting more deals in the pipeline via a bigger advertising and marketing spend.

It will also ensure they can adequately maintain and update the performance of their platform, so that new customers migrate to their solution.

And if they can do that, here’s an image of the total market size on offer:

With ONE contracting 7,307 out of 970,000 beds in the US (less than 1%), we believe ONE has ample room to grow.

They’ve established a foothold and given that their product can be delivered via the cloud we think it can take up more and more real estate in the US healthcare market.

The Uber strategy: a well known “land grab” case study in tech

Think of ONE’s “land grab” like this...

ONE is trying to grow its business in US healthcare the same way Uber grew its rideshare business.

It’s the same strategy, the same plan of attack. And it all comes back to making legacy services outdated quickly.

Uber provided a better service than taxis and solved a real world problem. So they decided to spend heavily on user growth and customer experience rather than becoming cash flow positive early on a small budget.

They ran rides at fares that were loss making in order to achieve scalability.

With clever marketing strategies and a clearly better service - it didn't matter to investors whether they were loss making in the near term, or not.

In the case of ONE, we think a similar strategy will work after today’s capital raise.

Increase marketing to grow the number of contracted beds in the US as quickly as possible and then we think the shareholder value will accrue to ONE over time.

This has a two-fold benefit in our eyes:

- With the capital raise in hand, ONE will spend to acquire a large number of sticky customers on the platform (customer retention rate of 98%)

- This move then limits competition risk at this early stage, because this is a footrace for users and speed is of the essence. Wait too long to grow contracted beds and a competitor can sneak onto the playing field.

As a result, we think ONE’s success will be judged predominantly on its user base or number of beds contracted, and how fast they can grow it - fast early growth will imply fast future growth.

We think this will be the catalyst to re-rate the ONE share price as new investors will value the company on a future recurring revenue multiple based on the early fast growth.

Which is why we’ve added the following new milestones to our original investment thesis for ONE:

🔲 Double marketing spend (check in next quarterly)

🔲 New USA deal #1 by Feb 2022

🔲 New USA deal #2 by April 2022

🔲 New USA deal #3 by June 2022

🔲 Reach 15,000 contracted beds within 9 months

🔲 Reach 20,000 contracted beds within 18 months

🔲 Cross selling and upselling - new products/integrations sold

(note: these are our personal opinion on what we would like to see as investors in ONE, they have now been added to our revised investment thesis on the ONE company page)

ONE calls its current sales strategy, ‘Land and Expand’ - land a deal with a hospital network, then increase the footprint or number of beds contracted within the network as quickly as possible.

Here is how we think adding marketing spend will improve the land and expand strategy:

But in order to fully execute this strategy it is very handy to have a constantly improving customer experience so those sticky customers stay sticky.

In other words, ONE needs to solve real-world problems and create an amazing experience for their client hospitals to drive word of mouth sales, which is critical in enterprise sales.

ONE’s problem to solve: Hospitals want to maximise the quality and volume of care using the same number of staff

There’s a compelling economic story behind what ONE is trying to achieve - namely, that the US is in the middle of a nursing labour shortage.

Nurses are getting overrun in the US due to high case numbers and legacy tech.

The combination of these two factors has led to the rise of travelling nurse agencies. The Associated Press recently outlined how average pay for a traveling nurse has gone from around US$1,000 to US$2,000 per week pre-pandemic to US$3,000 to US$5,000 now.

This is a classic example of what happens in a labour crunch.

Businesses spring up offering labour to the highest bidder.

Which has led to hospitals wanting to maximise the quality and volume of care using the same number of staff.

Rising labour costs generally lead to a desperate search for productivity and efficiency gains.

This is where ONE comes in and we think they have two brand-new products that can help address rapidly rising labour costs in US hospitals.

ONE announces new product integrations to help nurses maximise care: Cross-sell and upsell opportunities

In a recent presentation released to the ASX on Wednesday last week:

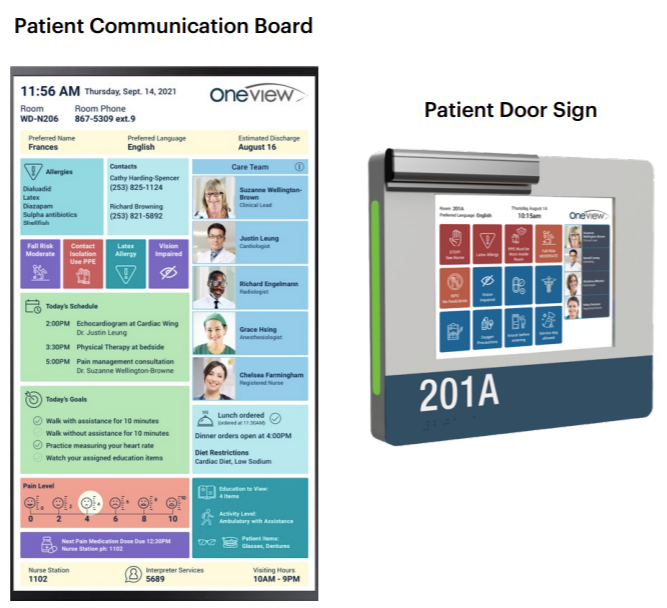

If you’ve been to a hospital recently, you’d likely have noticed outdated whiteboards on the outside of the beds and clipboards and pens (often not working) hanging by the bed.

Nurses frantically run around making notes, and the information on the boards is not always accurate or up to date.

ONE solves for this with a Patient Communication Board and a Patient Door Sign that integrates with ONE’s existing solutions.

Over time, we expect these new tech enhancements to provide cross-sell and upsell opportunities for ONE.

Got ONE’s first product? Well, here’s a suite of complementary products to really modernise your hospital and reduce the pressure on nurses.

We think that’s a good deal for hospitals that are squeezed and a good deal for ONE as well.

We believe the proceeds from today’s capital raise will go to rolling out these enhancements to existing client hospitals, in addition to upping their advertising and marketing spend.

Risks

The US is a lucrative market but convincing hospitals to change how they operate is no easy task. One of the key points CEO James Fitter made in a recent presentation is that hospital budgets are constrained in the current pandemic environment. So a key risk is ongoing budget pressure that prevents additional spend on ONE’s products. There’s a lot of inertia in the system and change may be slow initially.

While ONE’s early-mover advantage and the co-sell agreement with Microsoft via the Azure marketplace and the partnership with Samsung are valuable - competition and technology risks are important to consider. Other products may emerge that provide competition for ONE.

In an ideal world, ONE beats its revenue guidance and announces a flurry of new deals in the US. But if these deals take too long and ONE is quiet on the news front for a few months, impatient holders may lose interest in ONE and it could track sideways or downwards.

What we want to see next from ONE

When we first invested in ONE, management made it abundantly clear that the US market is the main goal.

So what we want to see next from ONE is increased marketing spend, getting key sales personnel onboard and deals flowing from that initiative, specifically in the US.

This should all lead into a strong uptick in user base growth.

We want to see them hit revenue guidance or beat it as well.

We think this is now a secondary consideration to how many contracted beds they manage to pick up after this capital raise (user base).

Here are the additional key milestones we looking for going forward:

Oneview Healthcare Company Milestones

✅ Portfolio Initiation

✅ Cloudcare Experience Launches on Time

📅 Jan-Mar Quarterly 2021 (Keep costs stable, increase revenue 20%)

📅 Apr-Jun Quarterly 2021

📅 FY2021 Results

📅 Double USA Revenue H1 2021

📅 Double USA Revenue H2 2021 (from H1 2021)

🔲 First New Customer via Samsung Partnership

✅ New "Expand" Deal signed (upsell deal with existing customer)

✅ First New Cloud Customer in Australia

✅ First New Cloud Customer in U.S

🔲 Initiation of research coverage by mainstream broker

🔲 Favourable Outcome in Regis Court Case

🔲 Multiple New Customers via Samsung Partnership

🔲 Multiple "Expand" Deal signed (upsell deal with existing customers

🔲 Multiple "Land" Deal Signed (small new customer deal with upsell potential)

✅ First New Customer via Microsoft Partnership

New Milestones Added (Post Cap Raise)

🔲 Double marketing spend (check in next quarterly)

🔲 New USA deal #1 by Feb 2022

🔲 New USA deal #2 by April 2022

🔲 New USA deal #3 by June 2022

🔲 Reach 15,000 contracted beds within 9 months

🔲 Reach 20,000 contracted beds within 18 months

🔲 Cross selling and upselling - new products/integrations sold

We think ONE management will use the money from the capital raise wisely.

ONE originally listed back in March 2016 and over the subsequent years raised capital twice ($30M in 2017 and a further $25.8M in 2019) - they spent this cash building out the product and getting the first deals, but there were some of hiccups along the way and delays in deals, as well as a much publicised legal dispute with aged care provider Regis.

At this stage in ONE’s trajectory we think it's good that they have successfully tapped the market for cash on two previous occasions, meanwhile learning important lessons about the product, the US market and how to get their product into hospitals.

Based on the previous lessons learned, we’re of the opinion that ONE will be good stewards of this fresh injection of capital to the business and that this is the right move for them to realise their US ambitions.

REMINDER: What is ONE and why we invested

In March, we invested in ONE and added them to our portfolio as our 2021 Tech Pick of the Year. Here are the ten reasons we gave for investing in ONE, you can see our deep dive into each reason in our original note here: 10 reasons we invested in ONE.

Here are the headline reasons:

- Great product for a hot sector - telehealth and health tech

- Established tech company that is undervalued (*our opinion was that ONE was undervalued when we first invested in March 2021)

- Board, management and shareholders all invested in the last round.

- The product looks really good

- Big Market: Growing need for virtual healthcare

- Market Traction: Hospital uptake continues to grow

- Profit margins expected to increase with continued moves to the cloud

- Partnership with Samsung

- Milestones and catalysts in 2021

- Right sector, right tech, right time.

Our journey with ONE so far...

In March 2021, we announced ONE as our Tech Pick of the Year for 2021.

A few weeks later, we provided our deep dive analysis that outlined the 10 reasons that we invested in ONE.

Then, later that month, we revealed how we expect ONE’s new cloud offering to turbocharge growth of new hospital clients, hospital beds and recurring revenue.

In April, ONE released its quarterly results demonstrating its progress. Revenue was up 64% on the prior year, while costs were down a massive 84%. It also reported that a number of clients had renewed their contracts, a sure sign of confidence in the company and its technology.

Progress continued in May, when New York based hospital NYU Langone, one of the top 10 best hospitals in the USA, delivered an hour long webinar on the benefits they are getting from ONE’s technology. You can watch clips from that webinar here, or read the transcript.

After having only launched its cloud offering in March, by June, ONE had secured a five year contract with Victoria's largest private health service, Epworth HealthCare, for all 1,440 of its beds.

Just eight days later, ONE announced its second cloud deal, this time with Northern Health in Melbourne — another important proof point that ONE’s cloud strategy was working.

In late-July, ONE (unsurprisingly) reported another quarter of strong growth, which proved to be much better than our expected milestones for the company.

In October, ONE announced a US $2.4M contract, leveraging Samsung and Microsoft partnerships - the Kingman deal.

As of today’s capital raise, ONE expects FY21 revenue expected to be between €9.5 ($14.9M) and €10.0m ($15.7M)

ONE is reporting Environmental, Social and Governance (ESG) disclosures and progress

Best in class ESG companies attract more capital, better customers and top talent – this leads to better shareholder returns over time - ONE discloses its ESG progress and improvements on a quarterly basis.

Investment milestones

ONE was the biggest initial investment we made to date. ONE has delivered several impressive announcements and is up over 500% since we first invested. Like we did with VUL after it delivered a number of material announcements and rose over 500%, we sold a small portion of our holding to recoup our initial investment. Our plan now is to hold the remaining position as the ONE continues to execute on its plan over the next few years.

✅ Initial Investment: @ 6c

✅ Initial Investment: @ 27c

✅ Price increases 500% from initial entry

🔲 Price increases 1000% from initial entry

🔲 Price increase 2000% from initial entry

🔲 12 Month Capital Gain Discount

✅ Free Carry

🔲 Take Profit

🔲 Hold remaining Position for next 2+ years

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and associated entities (including staff), own 8,142,871 ONE shares.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.