88% Revenue Growth for Vonex (ASX: VN8) - More Upside Ahead?

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

If there is a small cap company that has put in the hard yards to bring it to the cusp of being cash flow positive, it is Vonex Ltd (ASX: VN8).

The diversified telecommunications group’s growth trajectory is impressive. Its June quarter update featured the strongest operational and financial quarter the company has delivered since listing on the ASX.

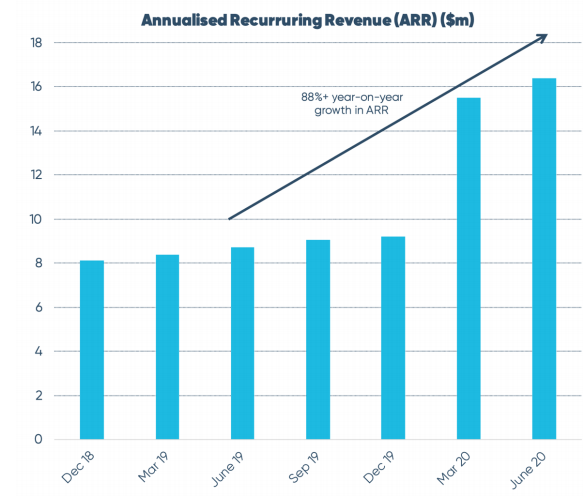

From an operational perspective, Vonex demonstrated an 88% increase in annualised recurring revenue during fiscal 2020 to $16.4 million.

The acquisition of 2SG has also been one of the company’s key achievements.

This acquisition has already provided Vonex with substantial sales momentum, with a full year contribution in fiscal 2021 likely to see the company generate robust growth in the next 12 months.

There have been plenty of benefits to come from the 2SG acquisition. Most notably, 2SG’s recent agreement to supply business grade mobile broadband to the $874 million capped ASX 300 company, Data#3 (ASX: DTL).

2SG is partnering with wi-fi solutions company Discovery Technology to enable the delivery of 4G and 5G network services, powered by Vonex, through to Discovery and the wider Data#3 customer base.

Discovery Technology delivers bespoke public Wi-Fi solutions to a broad range of industries including shopping centres, airports, universities, councils, smart cities, hotels, transport, retailers, supermarkets and stadiums.

Vonex’s activity highlight the company’s stability and resilience in trying times.

Of course it does operate in one of the sectors that looks to be as pandemic-proof as possible.

As IBM wrote in its Think Blog earlier this year, “Telecom operators have never been more relevant than they are today, connecting families and communities while keeping businesses and educational institutions logged on.

“During this unprecedented time, communication service providers (CSPs) have shown a resilience and willingness to act, giving us a glimpse into the new market reality. In this “new normal,” CSPs are leading the effort for remote working, online learning and social distancing.”

Telecommunications is the right sector at the right time and Vonex seems to be making all the right moves.

With recurring revenue providing forward earnings predictability, the coming 12 months could be the period of time in which Vonex really makes its mark on Australia’s small cap telco landscape.

So, let’s take a look at this growth in more detail and catch up with ...

Share Price: $0.11

Market Capitalisation: $20.43M

Cash at hand: ~$4.81 million (no debt) as of 30 June 2020

Here’s why I like VN8:

Vonex: a quick recap

For those unfamiliar with Vonex (ASX:VN8), this Brisbane-based award-winning telecommunications services provider sells fixed line, mobile, internet and hosted PBX and VoIP services to the small to medium enterprise (SME) market.

Vonex also offers white label NBN and 4G mobile broadband at wholesale rates.

Its crowning glory, should it make it to commercialising could be the Oper8tor App Vonex is currently developing. This is a multi-platform real-time voice, messaging and social media app that allows users to connect with all social media friends, followers and contacts across different social medias, all consolidated into one app.

In March this year, Vonex completed third party testing of the Operat8or app, however a commercialisation date is yet to be set. Importantly though, former CTO Angus Parker transitioned to Opert8or CEO and will work to speed up its progress to market.

Despite the delay to commercialisation of Oper8tor, Vonex has been charging ahead in 2020. In April, it recorded the strongest month in the company’s history for its Retail business.

Vonex hasn’t looked back.

You can read how Vonex got to this point in our previous articles:

- VN8’s New Qantas Partnership Presents Blue Sky Opportunity

- Vonex Share Price Set to Double, Says Analyst

We have been following the company since 2018, but it looks like 2020/21 could be its break out year.

The analysts think so

Analysts at PAC Partners believe there is significantly more upside in the Vonex story, with the broker setting its price target at 20 cents per share April 2020, representing a premium of 150% to the company’s share price at that time.

As 2020 has progressed, PAC Partners has cited Vonex’s strong operational performance and noted that the last capital raising boosted the group’s cash to nearly $5 million, leaving it well-placed to fund growth initiatives in fiscal 2021.

There are expectations that the number of registered users and customers on VN8’s PBX platform will expand through increasing channel partners and relationships like Qantas Business Rewards who have access to thousands of SMEs.

PAC Partners also anticipate average revenue per customer to increase through the sale of additional products and services, saying “The hero product to date has been ONDESK a hosted cloud solution, while in time the company will layer on NBN fibre, business-grade fibre and mobile services, with 5G expected to come via the Optus relationships acquired through the 2SG acquisition.’’

As for the NBN, PAC Partners said ‘’While NBN is reaching the end of the build, there are many premises ‘ready for service’ but not yet activated, so we see a positive industry backdrop for Vonex as these churn events create opportunities.

“We would also expect a big tail of activity just before the Core Access Network is turned off and SMEs are mandated to evaluate their telco services.”

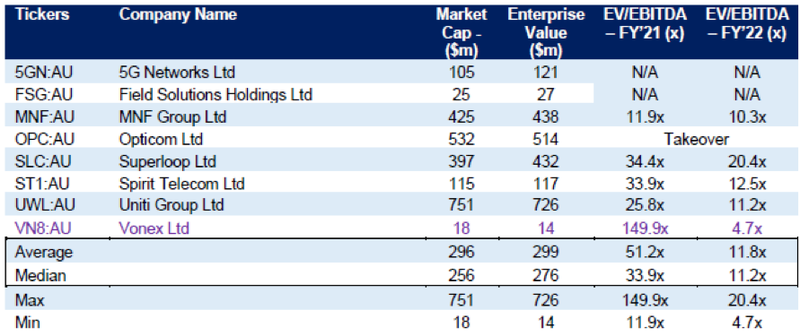

The analyst believes Vonex is undervalued, conducting a peer comparison on 9 July when its share price was 10 cents:

You can read a full PAC Partners appraisal in the following Finfeed article:

It’s all down to the growth

2020 is a bit of a highlight reel for Vonex.

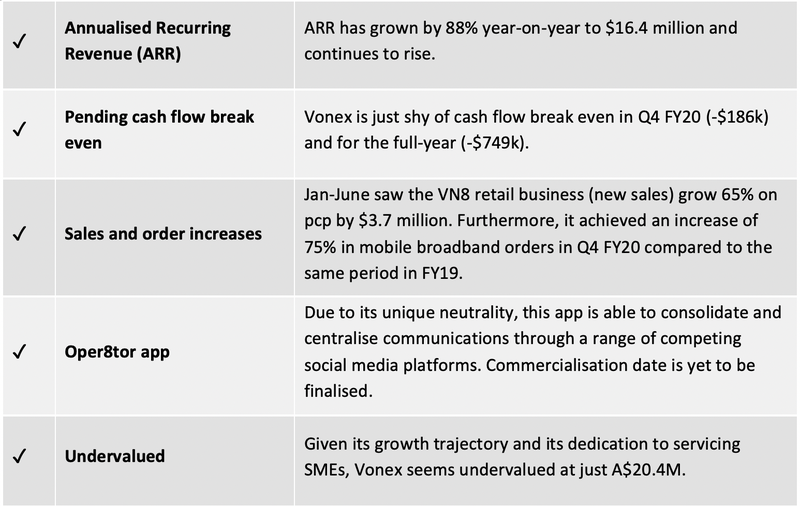

Highlights include:

- Business just shy of cash flow break even in Q4 FY20

- ARR now at $16.4M with momentum

- Jan-June saw the VN8 retail business (new sales) grow 65% on pcp by $3.7 million

- Agreement signed to supply business grade layer 2 mobile broadband to Discovery Technology

- 2SG is partnering with Discovery to enable the delivery of 4G and 5G network services, powered by Vonex, through to Discovery and wider Data#3 customers

- An increase of 75% in mobile broadband orders in Q4 FY20 compared to the same period in FY19

- Cash of $4.8m following a $1.4M placement and sale of Iron Ore Royalty Stream for the Koolyanobbing Iron Ore Project, which saw an initial cash inflow of $1.75M

Here’s a look at the annual recurring revenue:

The acquisition of 2SG has been an important and highly canny move by Vonex in terms of growth.

2SG Wholesale has brought a new dimension to the Vonex business. Vonex is now able to expand its offering to small and medium enterprise (SME) customers with new products including fleet mobile, mobile broadband and NBN with 4G backup.

2SG’s multi-year investment in a sophisticated network environment is also contributing to a meaningful relationship with Optus Wholesale, helping to build traffic on the Optus network by quickly deploying complex solutions for a broad base of customers.

Vonex plans to expand its network through direct integration to NBN points of interconnect in strategic national locations via 2SG Wholesale.

Building upon its existing points of interconnect and those it activated during the June quarter, Vonex now aims to improve its network quality by adding more direct interconnects with the NBN throughout fiscal 2021.

This streamlined supply chain provides customers with reduced lead times and enhanced assurance while positioning the company with the best possible commercial structure to leverage future wholesale NBN growth.

New business is good for business

Frequent customer wins are becoming the norm for Vonex.

This is, in part, due to the 2SG acquisition. However, overall operational strategy is also playing an important role.

Vonex has partnered with organisations of national scale as evidenced by the Data#3 win which related to the group’s Discovery Technology subsidiary.

This agreement involved the supply of business grade layer 2 mobile broadband to Discovery Technology which delivers bespoke public Wi-Fi solutions to a broad range of industries including shopping centres, airports, universities, councils, smart cities, hotels, transport, retailers, supermarkets and stadiums.

There is also growth in new customers and order value.

Vonex added five other new wholesale customers in May and June 2020, while also achieving an increase of 75% in mobile broadband orders in the June quarter compared to the same period in FY19.

This promising growth reflects achievement of the cross-selling opportunities which Vonex identified prior to acquiring 2SG Wholesale.

The Company has also scoped and commenced its plans to integrate 2SG Wholesale’s billing with Vonex’s existing platform, with completion expected in the December quarter.

Vonex will continue to pursue both organic and acquisition-led opportunities to grow its wholesale business in FY21.

Good news in retail

There is one good story in retail as COVID-19 continues to hurt the industry in some states.

Vonex’s retail operations are cranking, having achieved Total Contract Value of new customer sales in the six months from January to June 2020 of $3.7 million.

That is an increase of 65% on the previous corresponding period, with growth accelerating in the June quarter.

Vonex’s value proposition is thus resonating with its target market of Australian SMEs, many of which have been attracted by the company’s ability to rapidly provision scalable cloud-based business phone systems.

Excellent customer experience is a core component of its service offering and this seems to be differentiating it from the pack.

Furthermore, early July saw Vonex expand on its Qantas Business Rewards offering, adding mobile plans to the suite of services on which Qantas Points can be earned, with a view to gaining further market share with Australian SME customers.

We covered Vonex’s relationship with Qantas in our previous article.

The final word

After a successful capital raising in June, Vonex is well-placed to pursue a variety of growth initiatives.

With zero debt and cash of nearly $5 million as at 30 June 2020, it can now build on its growth trajectory and turn its attention to revenue generation that helps it become a cash flow positive telco, in what could be the new age of telecommunications.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.